Blockchain's Evolution: From Speculation to Financial Inclusion Catalyst

The Promise of Decentralized Finance

Financial inclusion, the effort to ensure individuals and businesses have access to useful and affordable financial products and services, remains one of the most significant global challenges. Billions still lack basic access to banking, credit, and insurance, perpetuating cycles of poverty and hindering economic development. Traditionally, addressing this gap has involved infrastructural improvements, policy changes, and the expansion of traditional banking networks. However, a new technological paradigm is emerging that promises to leapfrog these challenges: blockchain technology.

This article marks the first in a four-part series exploring how blockchain is moving beyond its speculative origins to become a foundational technology for financial innovation and inclusion. We will trace this evolution, focusing on its transition from a niche technology associated primarily with volatile cryptocurrencies to a robust, usable infrastructure capable of solving real-world financial problems. This introductory piece focuses squarely on the technological shift, the practical applications driving financial innovation, and the crucial regulatory environments shaping its adoption in major global economies.

The Technological Leap: From Crypto-Speculation to Financial Utility

The Genesis of Blockchain: Bitcoin and the Early Narrative

Blockchain technology was initially introduced to the world as the backbone of Bitcoin. Its fundamental innovation was simple yet revolutionary: a decentralized, immutable ledger system secured by cryptography and distributed across a network of computers. This solved the “double-spending” problem without relying on a central intermediary (like a bank), thereby creating “trustless” transactions.

In its early years (roughly 2009–2016), the public narrative surrounding blockchain was almost entirely dominated by cryptocurrency, particularly Bitcoin and later Ethereum. For many, blockchain was crypto, and its primary use case was either speculative asset trading or, for some early adopters, a philosophical rebellion against centralized fiat currency. This era, while critical for proving the technology’s viability in a high-stakes, adversarial environment, obscured its broader potential. Volatility, security breaches on exchanges, and the association with illicit activity often overshadowed the underlying utility of the distributed ledger technology (DLT) itself.

The Shift to Enterprise and Utility: Separating the Coin from the Chain

Around 2017, a noticeable pivot occurred. While cryptocurrency markets experienced explosive growth and subsequent corrections, researchers, financial institutions, and major technology companies began isolating the core DLT concept from the purely financial assets it underpinned. They realized that the fundamental properties of blockchain; immutability, transparency, security, and decentralization, were perfectly suited for modernizing fragmented and inefficient global financial systems.

Key technological advancements fueled this transition:

Evolution of Consensus Mechanisms

The evolution of blockchain technology has seen a necessary shift from the original Proof-of-Work (PoW) consensus mechanism used by Bitcoin which, while secure, is slow and energy-intensive. This move toward alternatives such as Proof-of-Stake (PoS), Delegated Proof-of-Stake (DPoS), and various forms of Practical Byzantine Fault Tolerance (PBFT) has driven significant improvements. These newer mechanisms offer much faster transaction finality (high throughput) and lower energy consumption, making them “faster” and “greener.”

These high-speed, eco-friendly chains are vital for enterprise-level applications that demand high volume, such as interbank settlements or the high-frequency micropayments required for financial inclusion initiatives. Among the leading platforms that are fast, green, and quantum-ready are Algorand, followed closely by Solana, Aptos, Hedera, and Stellar.

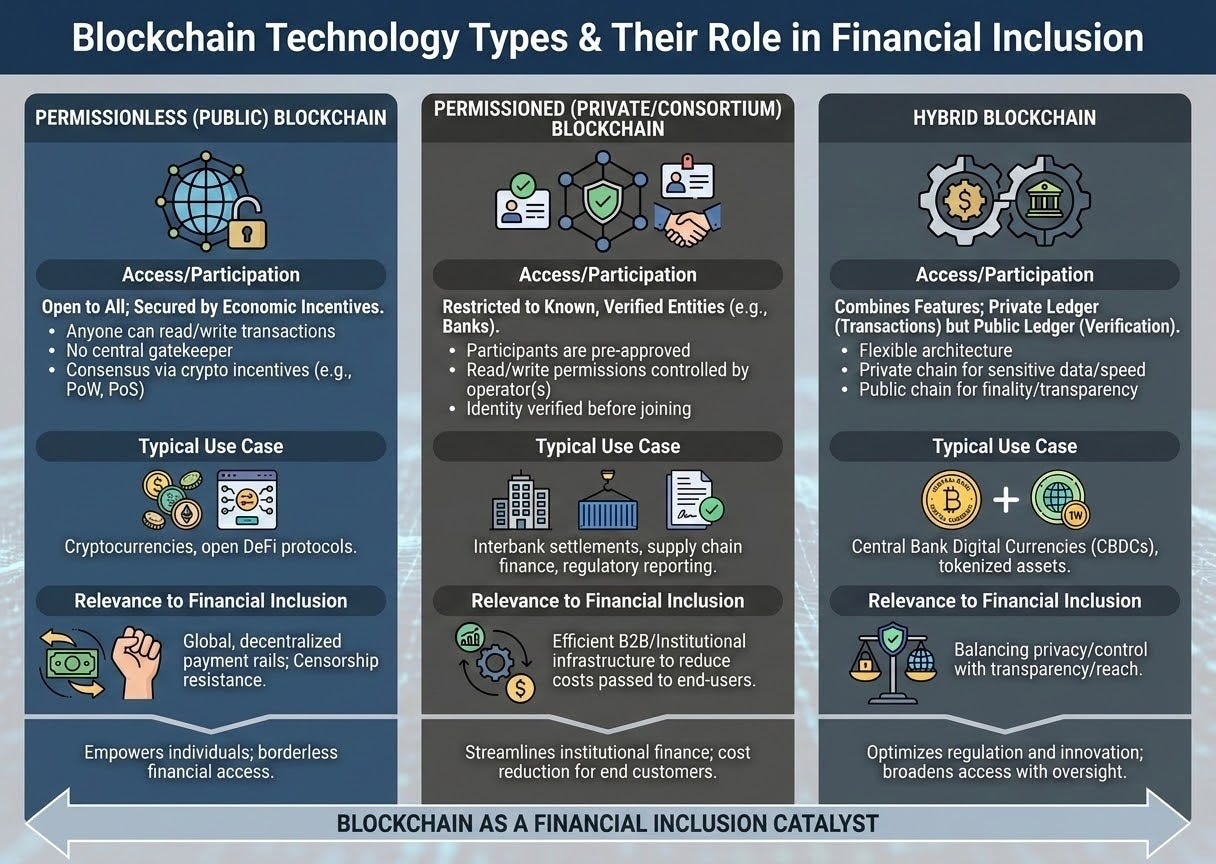

The Rise of Permissioned and Hybrid Blockchains

While the original blockchains were “permissionless” (anyone could join and validate transactions), financial institutions often require more control over who participates in the network, ensuring compliance with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations. This led to the development of permissioned blockchains (e.g., Hyperledger Fabric, R3 Corda), where access is restricted. These chains offer the benefits of DLT (shared single source of truth, immutability) while maintaining necessary governance, making them the preferred architecture for many corporate and governmental financial projects. Hybrid models, combining public access with private governance, are also gaining traction.

Blockchain as an Engine for Financial Inclusion

The core capabilities of DLT directly address the historical barriers to financial inclusion:

Cost Reduction: By removing intermediaries and automating processes (via smart contracts), DLT significantly lowers the cost of cross-border remittances, credit servicing, and account maintenance, making it economically viable to serve low-income populations.

Identity and Credit Access: For the unbanked, a lack of verifiable identity or credit history is a major hurdle. Blockchain can host tamper-proof digital identities (Self-Sovereign Identity, SSI) and verifiable transaction histories, creating a basis for credit scoring where none existed before.

Accessibility and Reach: A smartphone with an internet connection is often the only requirement to interact with a blockchain-based financial service. This bypasses the need for expensive physical bank branches and ATMs, extending services into remote areas.

Transparency and Trust: The transparent and immutable nature of the ledger increases trust in transactions and allows for faster, more effective tracking of aid, micro-loans, or social benefit payments, ensuring funds reach the intended recipients.

The Evolving Global Regulatory Landscape

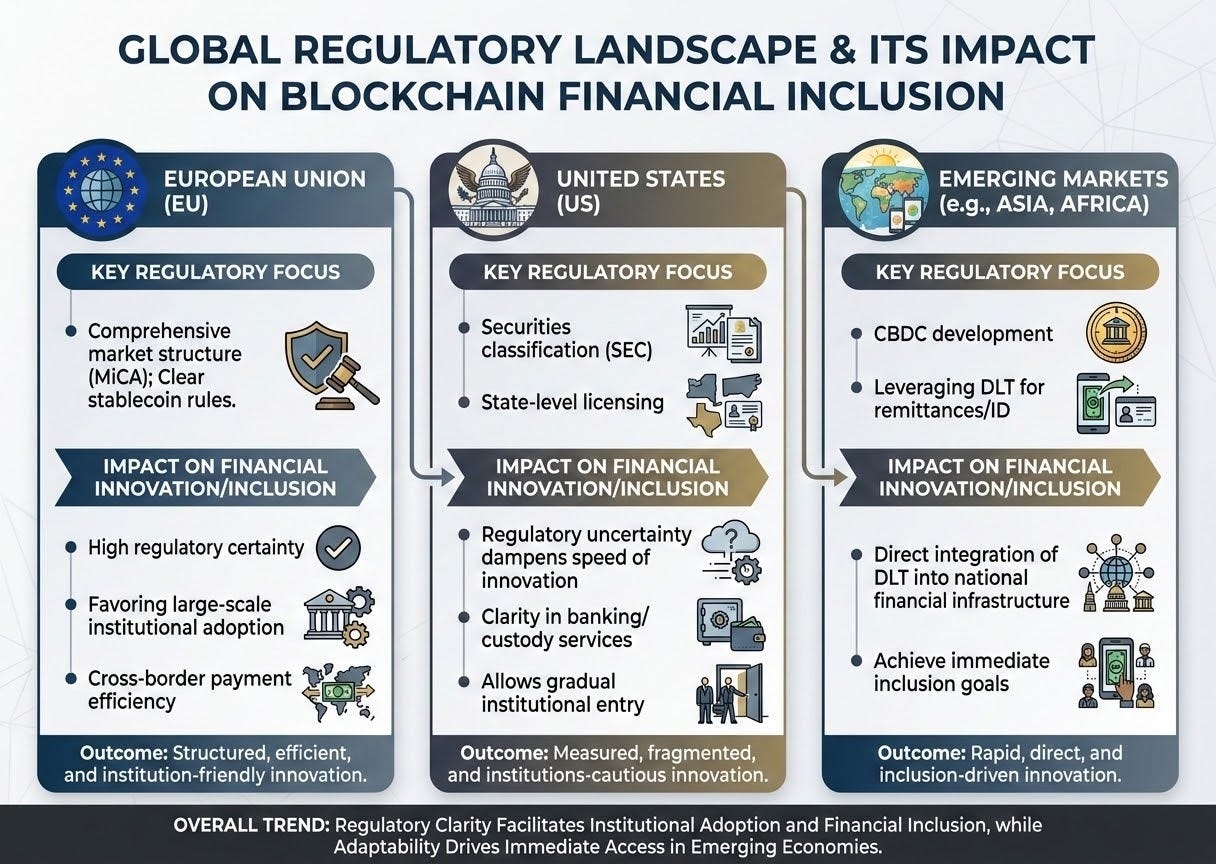

The transition of blockchain from a speculative tool to a financial utility has placed it squarely in the sights of global regulators. The challenge is immense: how to harness the technology’s benefits—efficiency, speed, inclusion—while mitigating its inherent risks—money laundering, consumer protection, and systemic stability. Three major areas—the European Union, the United States, and emerging economies—illustrate the diverse approaches being taken.

The European Union: Prioritizing Legal Clarity and Market Structure

The European Union has often taken a proactive, comprehensive approach to DLT regulation, seeking to create a harmonized framework across its 27 member states.

The Markets in Crypto-Assets (MiCA) Regulation

MiCA is arguably the most ambitious and sweeping regulatory framework globally. Adopted in 2023, its aim is to provide legal certainty for crypto-asset issuers and service providers (CASPs) operating within the EU. Key components of MiCA include:

Categorization: Defining three main types of crypto-assets: asset-referenced tokens (ARTs), e-money tokens (EMTs), and utility tokens.

Licensing and Authorization: CASPs (e.g., exchanges, custodians) must be authorized by a national competent authority, establishing capital requirements and governance rules similar to traditional financial institutions.

Consumer Protection: Imposing strict transparency and disclosure requirements on issuers, particularly for stablecoins (ARTs and EMTs), ensuring adequate reserve backing.

MiCA’s focus on defining clear rules for stablecoins (which are vital for cross-border financial inclusion payments) and service providers is crucial for fostering institutional trust and allowing blockchain-based financial services to scale across the EU market.

Pilot Regime for Market Infrastructures

Alongside MiCA, the EU introduced a DLT Pilot Regime, allowing financial institutions to temporarily operate DLT-based market infrastructures (like trading and settlement systems) under lighter regulation. This sandbox approach is designed to test how tokenized securities and other innovative financial instruments can function safely within existing financial regulation.

The United States: A Patchwork of Regulation and Enforcement

The regulatory environment in the U.S. is notably more complex, characterized by overlapping jurisdictions (SEC, CFTC, Treasury, state regulators) and a “regulation by enforcement” approach, particularly concerning crypto-assets.

The Securities and Exchange Commission (SEC) Stance

The central debate in the U.S. revolves around which crypto-assets constitute “securities” and are therefore subject to SEC jurisdiction. The SEC relies heavily on the Howey Test to determine if an asset is an investment contract. This has created significant legal uncertainty, with the SEC pursuing enforcement actions against major exchanges and issuers. While this focus aims to protect investors, the lack of clear legislative guidance has been cited as a hindrance to innovation, prompting many DLT firms to explore jurisdictions with more explicit rules.

Banking and Payment Clarity

Conversely, other U.S. bodies have been more forward-looking regarding the underlying technology. The Office of the Comptroller of the Currency (OCC) has previously issued interpretive letters clarifying that national banks can use stablecoins and public blockchains for payment and settlement activities, and can offer crypto custody services. At the state level, initiatives like New York’s “BitLicense” offer specific operational frameworks, albeit often criticized for being overly restrictive.

The U.S. approach is moving toward clarity, but through multiple legislative proposals rather than a single unified framework like MiCA, resulting in slower, more fragmented adoption of DLT for mainstream finance.

Similarly Important Economies: Asia and Emerging Markets

While the West grapples with regulatory clarity, nations across Asia and the developing world are often leading the way in integrating DLT into national financial infrastructure, driven partly by the acute need for better financial inclusion tools.

Central Bank Digital Currencies (CBDCs)

A defining trend globally is the experimentation with CBDCs. China’s digital Yuan (e-CNY) is the most advanced, being extensively piloted for domestic use. The technology underpinning many CBDC trials is DLT or DLT-inspired. CBDCs offer a state-backed, risk-free digital currency that can operate on a DLT rail, dramatically improving the efficiency of government payments, aid distribution, and domestic financial inclusion. Other nations, including India (e-Rupee) and Nigeria (e-Naira), are also actively deploying or piloting CBDCs, leveraging the inherent efficiencies of a digital ledger system.

Regulatory Innovation in Financial Hubs

Jurisdictions like Singapore and the UAE (particularly Dubai) have sought to position themselves as global DLT hubs by creating pragmatic regulatory sandboxes and clear licensing regimes for Virtual Asset Service Providers (VASPs). Singapore’s Payment Services Act, for instance, provides a framework for payment token service providers, allowing firms to test new inclusion models without fear of sudden regulatory shifts. This targeted regulatory innovation is attracting significant investment and development, proving that thoughtful regulation can accelerate, rather than stifle, adoption.

Practical Applications Driving Financial Inclusion

The move away from speculation is best evidenced by the concrete, usable applications of DLT being deployed today, directly targeting the unbanked and underserved.

Remittances and Cross-Border Payments

The global remittance market—a lifeline for many developing countries—is notoriously slow and expensive, often costing 5–10% of the principal amount. Blockchain solutions drastically cut these costs and speeds.

DLT providers utilize cryptocurrency or stablecoins as a transfer layer, bypassing correspondent banking networks. For example, a worker can send funds that are instantly converted to a stablecoin, transferred over a public or permissioned blockchain network in minutes, and converted back into local currency at the receiving end. This efficiency directly increases the usable income for recipients and fosters trust in digital payment systems.

Decentralized Identity and Credit Scoring

For millions, the barrier to finance is the lack of a government-issued ID or a verifiable financial history.

Self-Sovereign Identity (SSI): SSI models use blockchain to give individuals control over their digital credentials. Instead of storing data in a centralized database (which can be hacked or denied), the blockchain stores only cryptographic proofs, while the user holds their private data. They choose who sees what data. This immutable digital ID is the key to unlocking basic services—bank accounts, healthcare, and education—for the previously invisible population.

Credit History: Blockchain can record micro-transactions, utility payments, and participation in peer-to-peer lending programs as verifiable, non-custodial data points. This creates a legitimate credit history for individuals excluded from traditional systems, enabling access to micro-loans and small business financing.

Tokenization of Real-World Assets (RWA)

Tokenization involves representing ownership of a tangible asset (like real estate, art, or commodities) or an intangible asset (like securities or debt) as a digital token on a blockchain. This has immense potential for inclusion:

Fractional Ownership: Tokenization allows large, illiquid assets (like a commercial property) to be divided into thousands of small, affordable tokens. This democratizes investment, allowing individuals with minimal savings to participate in asset classes previously reserved for the wealthy.

Liquidity: Tokens can be traded 24/7 on global exchanges, significantly increasing the liquidity of assets in emerging markets, which often suffer from illiquid local financial markets.

Conclusion: Setting the Stage for the Future of Finance

The journey of blockchain has been a remarkable one, transitioning from a conceptual curiosity tied to volatile assets into a robust, enterprise-grade technology ready to underpin the next generation of global financial infrastructure. The utility-driven focus—cost reduction, identity verification, and efficient settlements—is directly aligned with the imperative of financial inclusion.

While regulatory challenges persist, particularly in achieving a unified global approach, the creation of clear frameworks like MiCA and the rapid deployment of applications in areas like remittances and digital identity confirm the shift: blockchain is no longer a technology for speculation, but a technology for financial innovation and societal betterment.

The subsequent articles in this series will delve deeper into the specific organizations and protocols—both public and private—that are leveraging this technology to deliver concrete, scalable financial solutions to the underserved populations around the world, making the promise of financial inclusion a tangible reality.

Citations and Sources

This section provides citations for the claims and statistics presented in the article.

General Financial Inclusion Data

Billions still lack basic access to banking, credit, and insurance.

The Technological Leap

Description of blockchain’s core innovation, solving the “double-spending” problem.

Reference to Proof-of-Work (PoW) versus Proof-of-Stake (PoS) consensus mechanisms.

Mention of permissioned blockchains like Hyperledger Fabric and R3 Corda used by financial institutions.

DLT reducing the cost of cross-border remittances.

The Evolving Global Regulatory Landscape

MiCA (Markets in Crypto-Assets) Regulation adoption date and key provisions (Categorization, Licensing, Consumer Protection).

DLT Pilot Regime establishment.

SEC reliance on the Howey Test for defining securities.

OCC interpretive letters regarding stablecoins and public blockchains for national banks.

China’s digital Yuan (e-CNY) being extensively piloted; India (e-Rupee) and Nigeria (e-Naira) actively piloting CBDCs.

Singapore’s position as a DLT hub and the Payment Services Act.

Practical Applications

Global remittance market often costing 5–10% of the principal amount.

Decentralized Identity / Self-Sovereign Identity (SSI) models leveraging blockchain.

Tokenization of Real-World Assets (RWA) and fractional ownership.

It analyzes how blockchain shifted from the speculative hype of 2017-2021 to a mature consolidation phase, where public interest dropped but developers kept building. Great content!!