The Tech That Lowers the Walls: How Next-Gen Blockchain Solves for Inclusion

Privacy, Performance, and the Architecture for Equitable Finance.

In our previous exploration, “Blockchain’s Evolution from Speculation,” we traced the arc of distributed ledger technology from its roots as a niche tool for digital gold to its current status as an enterprise-grade utility. We concluded that the “Walled Garden” of global finance—a system optimized for the wealthy but exclusionary for billions—is finally meeting its architectural match.

But identifying the problem is only half the battle. To truly dismantle the extractive gates of the legacy system, we must look at the specific, “next-gen” technological breakthroughs that are moving from research papers to real-world applications. We are moving beyond the era of “crypto hype” and into the era of financial utility. This isn’t just about moving pixels; it’s about moving prosperity. It is about a technological imperative that leverages decentralization to create a foundational financial layer that is borderless, permissionless, and inherently equitable.

The High Cost of Being Underbanked

To understand the solution, we must first confront the sheer brutality of the status quo. The common misconception is that financial exclusion is solely a problem of the developing world. The data tells a different story. While roughly 1.4 billion adults worldwide remain unbanked, wealthy nations like the U.S. and the EU grapple with a “crisis of access”.

In the United States, the underbanked—disproportionately composed of Black, Hispanic, and Low-to-Moderate Income (LMI) households—are diverted into Alternative Financial Services (AFS). These services, such as payday loans, operate on a predatory model with Annual Percentage Rates (APRs) often reaching 300% to 400%. This is not a service fee; it is a “Poverty Tax”—a structural wealth drain that strips tens of billions of dollars annually from the communities that need it most.

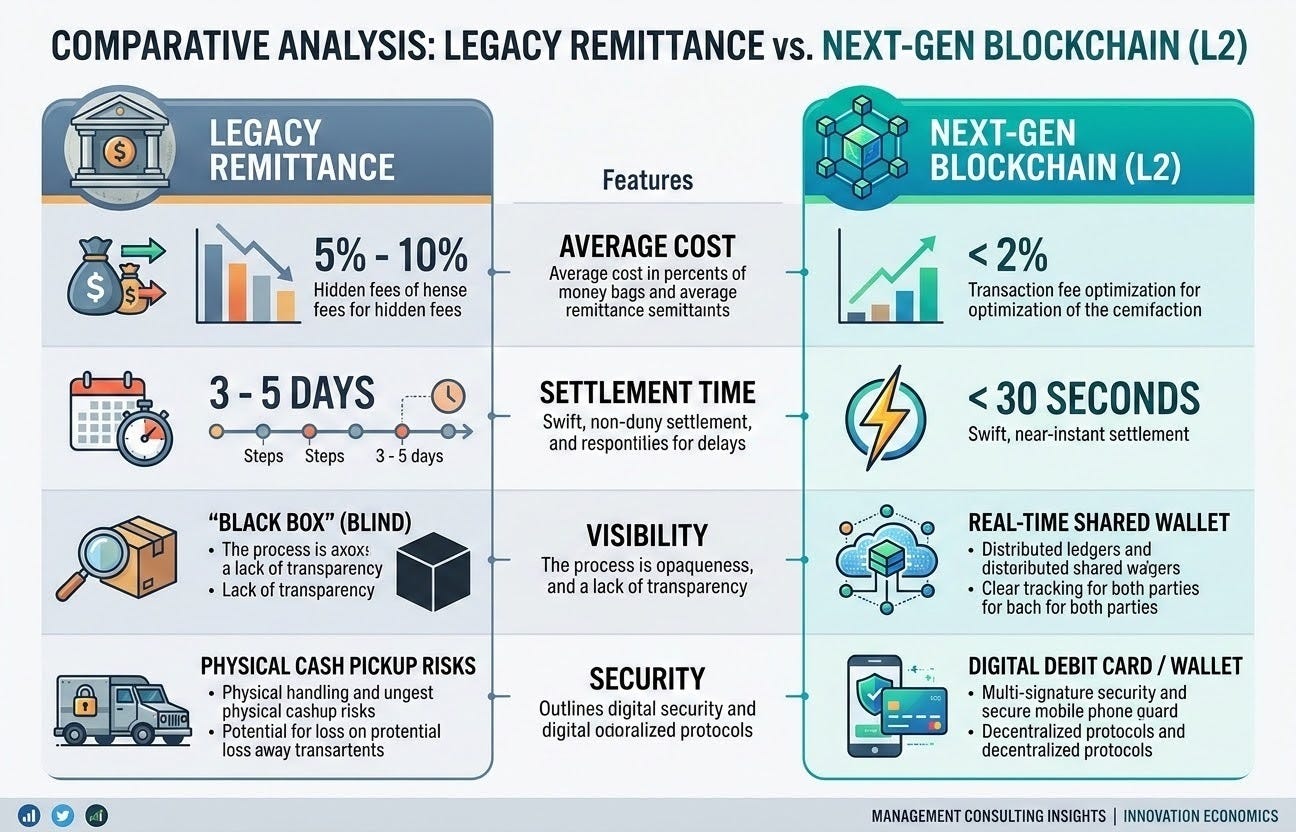

Similarly, Europe faces a $1 trillion economic failure rooted in cross-border fragmentation and exorbitant remittance costs. When a migrant worker in Paris sends money to family in Dakar or Bogota, they often lose 5% to 10% of their hard-earned wages to hidden FX markups and intermediary fees. For someone earning minimum wage, a $40 fee on a $500 transfer represents approximately five hours of labor lost to the “black box” of legacy infrastructure.

The legacy system is like a highway where the toll booth takes 10% of your car’s value every ten miles. Next-gen blockchain tech is the bypass.

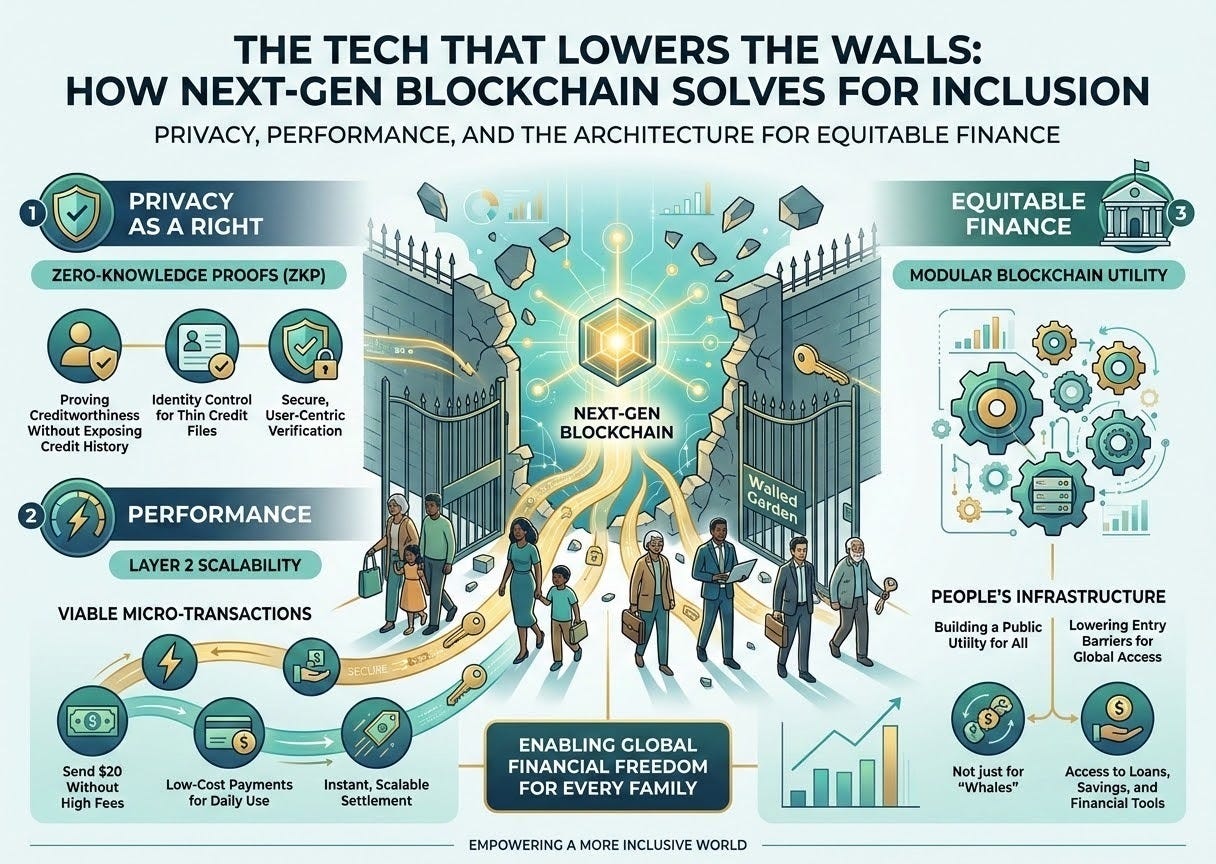

Privacy as a Right, Not a Luxury

One of the most significant barriers to inclusion is the “Credit Catch-22.” To get credit, you need a credit history. But if you are among the “credit invisible”—those with thin or non-existent files at centralized bureaus—you are locked out. Traditional underwriting relies on opaque, historical risk models that often default to denial for marginalized populations.

Enter Zero-Knowledge Proofs (ZKPs)

Zero-Knowledge Proofs are perhaps the most “magical” technological breakthrough in recent cryptography. In simple terms, a ZKP allows you to prove that a statement is true without revealing the data that makes it true.

Think of it like this: If the traditional financial system wants to know if you can afford a loan, they demand your entire financial history, your social security number, and your address—essentially asking to see your entire house just to prove you have a kitchen. A ZKP allows you to show a “green light” that proves you meet the income requirements without sharing a single sensitive data point.

For the underbanked, this is revolutionary:

Creditworthiness Without Exposure: Users can prove they have consistently paid rent or utilities—routine payments the FICO system ignores—using cryptographically verifiable proofs.

Self-Sovereign Identity (SSI): Blockchain can host tamper-proof digital identities where the user, not a government or bank, owns their credentials. This removes identification hurdles for immigrants and mobile citizens who lack traditional documentation.

Privacy-Preserving Compliance: Financial protocols can verify that a user is not on a sanctions list (AML/KYC compliance) without the protocol ever “seeing” the user’s private ID.

By shifting the power dynamic of data ownership, ZKPs transform privacy from a luxury for the paranoid into a fundamental tool for economic empowerment.

Speeding Up the Rails: Layer 2 and the $20 Micro-Transaction

The early days of blockchain were plagued by “gas fees”—the cost to process a transaction. During peak times, sending $20 on a legacy chain might cost $15 in fees. For a family trying to manage a tight budget, this is just as predatory as the legacy banking system’s overdraft fees.

The Viability of Micro-Transactions

Layer 2 (L2) scalability solutions are the answer to this bottleneck. L2s sit on top of foundational blockchains (like Ethereum), bundling thousands of transactions together and processing them off-chain before settling a single proof back to the main layer.

The result? The marginal cost of a transaction drops toward zero. This enables a shift from “one-off emergency transfers” to “recurring family budgeting”. Platforms like Latitud are already leveraging these efficient rails (such as Algorand) to offer near-instant settlement at a fraction of the cost of traditional wire services.

By making it economically viable to send $20 or $50, we unlock “Money Sharing” rather than just “Money Remitting”. Families can use sub-accounts to provision specific funds for groceries, medicine, or utilities, turning a fleeting transaction into a stable, daily financial relationship.

Building the People’s Infrastructure

For too long, the financial “stack” has been a series of silos owned by private interests. Modular blockchains are changing this by splitting the functions of a blockchain—execution, settlement, and data availability—into separate, specialized layers.

This modularity allows for the creation of a public utility infrastructure. Just as the internet protocol (TCP/IP) is a public good that anyone can build on, modular blockchain layers provide a transparent, immutable foundation for financial services.

Why “Modular” Matters for Inclusion:

Lower Entry Barriers: Entrepreneurs don’t need to build a whole bank; they can “plug in” to existing identity and payment modules.

Regulation as Code: Compliance rules (like the EU’s MiCA) can be embedded directly into the code layer. This ensures that protection for consumers is technically enforced rather than just legally promised.

Interoperability: A modular system ensures that a digital identity created in the U.S. can be verified by a micro-loan protocol in Latin America without friction.

We are moving away from a system where “trust” is something you buy from an expensive intermediary and toward a system where “trust” is an inherent property of the network architecture.

Conclusion: The Sovereign Future

Financial inclusion is the defining mission of our era because it forces us to confront the core injustices of the legacy system. It is a moral necessity to lift the millions of underbanked into full economic participation, and it is a monumental economic opportunity—a multi-trillion-dollar market currently held hostage by systemic inefficiency.

The “Next-Gen” technology we’ve discussed—Zero-Knowledge Proofs, Layer 2 scalability, and Modular architectures—provides the first credible pathway to a human-centric financial operating system. By construction, these tools favor the individual over the institution, and the participant over the gatekeeper.

The walls are finally coming down. The question is no longer if technology can solve for inclusion, but how quickly we can build the bridges to let everyone in.

Citations and Sources

World Bank Group. (2022). The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19. https://globalfindex.worldbank.org/

International Monetary Fund (IMF). Staff Discussion Notes on Financial Inclusion. https://www.imf.org/en/Publications/Search?series=Staff+Discussion+Notes&publicationtype=Staff+Discussion+Notes&Topics=Financial+Inclusion

Consumer Financial Protection Bureau (CFPB). Research and Reports. https://www.consumerfinance.gov/data-research/research-reports/

Federal Deposit Insurance Corporation (FDIC). Household Survey on Banking and Financial Services. https://www.fdic.gov/analysis/household-survey/

World Bank Group. (Ongoing). Remittance Prices Worldwide (RPW) Database.

The Brookings Institution. Economic Policy Research. https://www.brookings.edu/topic/economic-policy/

European Commission. SME Definition and Policy. https://ec.europa.eu/growth/smes/sme-definition_en

Nakamoto, S. (2008). Bitcoin: A Peer-to-Peer Electronic Cash System. https://bitcoin.org/bitcoin.pdf

Ethereum Foundation. (Ongoing). Consensus Mechanisms. https://ethereum.org/en/developers/docs/consensus-mechanisms/

European Parliament. (2023). Regulation (EU) 2023/1114 on Markets in Crypto-assets (MiCA). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32023R1114

Decentralized Identity Foundation (DIF). Core Specifications and Architecture Reports. https://identity.foundation/

McKinsey & Company. (2023). Tokenization: A digital-asset déjà vu. https://www.mckinsey.com/industries/financial-services/our-insights/tokenization-a-digital-asset-deja-vu