Breaking the Walled Garden

The End of Extractive Finance

Why Financial Inclusion is the Defining Mission of Our Era

For the past year, I’ve been dissecting the global financial system—not as a bystander, but as someone who has navigated its complex machinery and seen exactly who it serves, and who it excludes. The brutal truth is that the modern financial system is a walled garden. It is brilliantly optimized for those already inside—those with wealth, credit history, and the right passport—but it systematically locks out billions of adults worldwide.

The common misconception is that financial exclusion is a problem only of the developing world. We have previously explored how, in the U.S., it is a crisis of equitable access for marginalized households, driven by discriminatory lending, high fees, and the predatory logic of alternative financial services. Similarly, the European Union, often viewed as a beacon of modern policy, grapples with the Digital Euro Dilemma—a topic we explored in-depth in The Digital Euro Dilemma: Why Web3—and a hidden $1 trillion failure rooted in cross-border fragmentation, exorbitant remittance costs, and a crushing liquidity crisis for Small and Medium-sized Enterprises (SMEs).

This article is the culmination of that work, presenting the definitive argument for why Financial Inclusion is not just a social good, but the singular, most defining—and lucrative—economic and technological mission of our time. The required solution is not an incremental fix, but a complete bypass of the legacy system. The answer lies in the Web3 Imperative: leveraging decentralized technology to create a foundational financial layer that is borderless, permissionless, and inherently equitable. As explored in our first piece, The Future of Banking Isn’t a Bank, this new architecture is the only pathway capable of converting the estimated $1 trillion in systemic inefficiency identified in Europe, coupled with the hundreds of billions lost to predatory services in the U.S. and globally, into genuine, sovereign wealth for citizens and businesses across the globe. This total addressable market (TAM) is what we first analyzed in The $250 Billion Opportunity.

I. The Global Cost and Importance of Financial Inclusion: The Universal Drag

Financial inclusion, at its core, is the availability and equality of access to essential financial products and services—transactions, payments, savings, credit, and insurance—delivered affordably and responsibly. It is the fundamental foundation for dignified economic participation and the engine of sustainable development. Without inclusion, progress stalls, and poverty deepens, creating a universal drag on the global economy.

A. A Universal Problem with a Staggering Global Impact

The sheer scale of financial exclusion remains staggering, despite recent efforts to increase account ownership worldwide. Roughly 1.4 billion adults worldwide remain completely unbanked, representing about one-third of the global adult population. While 69% of adults globally now possess a transaction account, this statistic masks the pervasive problem of the ‘underbanked’. These are individuals who may technically hold an account, but it is often too expensive, too limited in functionality, or geographically inaccessible to be truly useful for building lasting financial resilience. They are effectively denied access to affordable credit, reliable insurance, and the ability to build a verifiable financial history, trapping them beneath a low ceiling of economic potential.

This exclusion is far more than a social inconvenience; it is a massive economic drain that hinders global prosperity and actively fosters instability. When billions are locked out, their potential for saving, investing, and accessing affordable capital is systematically suppressed. Studies consistently affirm that boosting financial inclusion is positively correlated with GDP growth, with the potential to increase it by up to 14% in developing economies alone. This growth is catalyzed by several crucial mechanisms:

Increased Entrepreneurship and Job Creation:

Access to basic, affordable financial tools, such as micro-credit and low-cost payment services, allows aspiring entrepreneurs to start, sustain, and scale small businesses. This grassroots economic activity stimulates local economies and is the most reliable engine for creating sustainable jobs within underserved communities.

Enhanced Risk Mitigation and Resilience:

Affordable insurance products, ranging from health coverage to crop insurance, act as essential safety nets. They protect vulnerable families and businesses from sudden, catastrophic shocks—like severe illness, crop failure, or natural disasters—which often force households into desperate debt and a downward spiral back into abject poverty.

Accelerated Capital Formation and Investment:

Secure, reliable savings mechanisms transform idle or hidden cash into productive capital within the formal financial system. Banks and financial institutions can then lend out this aggregated capital, lowering borrowing costs and fueling broader economic growth and investment cycles.

The core failure of the traditional financial system—the “walled garden”—is that its foundational architecture prioritizes extraction and control over universal access. Every mandatory fee, every high minimum balance requirement, every complex Know Your Customer (KYC) barrier, and every rigid geographic boundary functions as a deliberate gatekeeper. This structure ensures that wealth predominantly circulates among the already wealthy. The ultimate global challenge is not merely to build higher walls, but to dismantle these extractive gates entirely, which is the precise goal of the Web3 Imperative: to eliminate the need for the gatekeeper, creating a financial layer as ubiquitous, open, and efficient as the internet itself.

B. The Moral and Stability Imperative

Beyond the massive economic case, financial exclusion constitutes a profound moral crisis. It acts as a structural reinforcement of global inequality, systematically trapping entire generations in cycles of poverty from which escape becomes increasingly difficult. When people lack the ability to transact safely, save securely, or access credit affordably, they are forced to rely on informal, often dangerous, and invariably high-cost mechanisms. This deep lack of financial resilience contributes directly to social unrest, political instability, and massive humanitarian costs. A global system that actively marginalizes two billion potential participants is, by definition, an inherently insecure system. True global stability can only be achieved through widespread economic empowerment, and that empowerment must begin with the foundation of financial inclusion. The technological breakthroughs of the 21st century, specifically decentralized technology, have effectively removed any credible technical excuse for this continued exclusion; the challenge is now purely one of political will and architectural redesign.

II. The Financial Fault Lines in Developed Economies: The Crisis of Access and Equity

The fight for financial inclusion is not exclusively a distant problem for emerging markets; it is a profound and pressing domestic crisis at the heart of the world’s wealthiest economies. In these developed nations, the struggle is typically not against a complete absence of banks, but against subtle, systemic inequities and structural failures that prevent fair access and equal opportunity for all citizens.

A. The American Divide: Access vs. Equity

In the United States, the crisis is defined less by a lack of bank accounts and more by a lack of usable and affordable ones. The nation’s underbanked population—a group disproportionately composed of Black, Hispanic, Native American, and Low-to-Moderate Income (LMI) households—is systematically diverted into high-cost Alternative Financial Services (AFS) such as payday loans, title loans, and check cashers. This phenomenon is driven by deep-seated structural barriers:

The Poverty Tax and Systemic Wealth Extraction:

The underbanked are trapped in AFS that operate on a predatory, extractive model. Payday lenders, for example, charge rates equivalent to an Annual Percentage Rate (APR) of 300% to 400% on a typical two-week loan. This is not merely a high service fee; it is a structural wealth drain—a poverty tax—that guarantees systemic economic fragility. This tax strips tens of billions of dollars annually from the communities that need capital the most, diverting money that should be used for savings, education, and upward mobility. Furthermore, many LMI households are pushed out of the traditional banking system entirely because they cannot maintain minimum balances, leading to account closures due to excessive overdraft fees, further cementing their reliance on AFS.

Algorithmic and Geographic Discrimination:

Affordable credit is disproportionately denied to marginalized communities due to opaque and biased risk models and reliance on historical credit scores. If a person or community lacks a history of borrowing from traditional, privileged institutions—a common reality in immigrant or low-income neighborhoods—the underwriting algorithm defaults to denial or levies exorbitant rates. This institutional bias is compounded by the persistent legacy of redlining, which manifests today through the strategic closure of traditional bank branches in low-income areas and the simultaneous proliferation of AFS storefronts in these very same “banking deserts”.

Identification Hurdles and the Remittance Tax:

For many immigrant families, documentation hurdles significantly complicate the simple act of opening a standard bank account. Even when they successfully navigate these hurdles, the critical process of sending money back to their families abroad—a vital economic lifeline—remains prohibitively expensive. The exorbitant fees charged by traditional banks and legacy money transfer services cement reliance on high-cost, non-bank alternatives, further bleeding their earnings through the “remittance tax”.

The Web3 Solution offers a direct, surgical response to these pervasive structural failures. Decentralized Identity (DID) and on-chain credit scoring can completely bypass the need for traditional, biased documentation and opaque, exclusionary scoring models. A self-sovereign digital identity can unlock immediate access to financial services for those lacking traditional documentation. Crucially, Web3 enables the tokenization of verifiable, routine payment streams—such as consistent rent or utility payments, which are routinely ignored by the FICO system—allowing individuals to build a robust, portable credit profile entirely outside of the exclusionary legacy architecture. This empowers citizens to build wealth on their own terms, directly confronting centuries-old institutional barriers to financial equity.

B. The European Fragmentation: The $1 Trillion Failure

Europe’s structural financial problem is distinct from America’s but equally destructive: it is a chronic, policy-induced fragmentation that actively undermines the Single Market’s true economic potential. The excessive cost, slowness, and complexity of financial transactions across internal and external borders act as a systemic brake on continental economic activity. This results in a hidden, cumulative inefficiency that economic analysts conservatively estimate to be in the range of a $1 trillion lost economic opportunity.

The Border Tax and Remittance Drain:

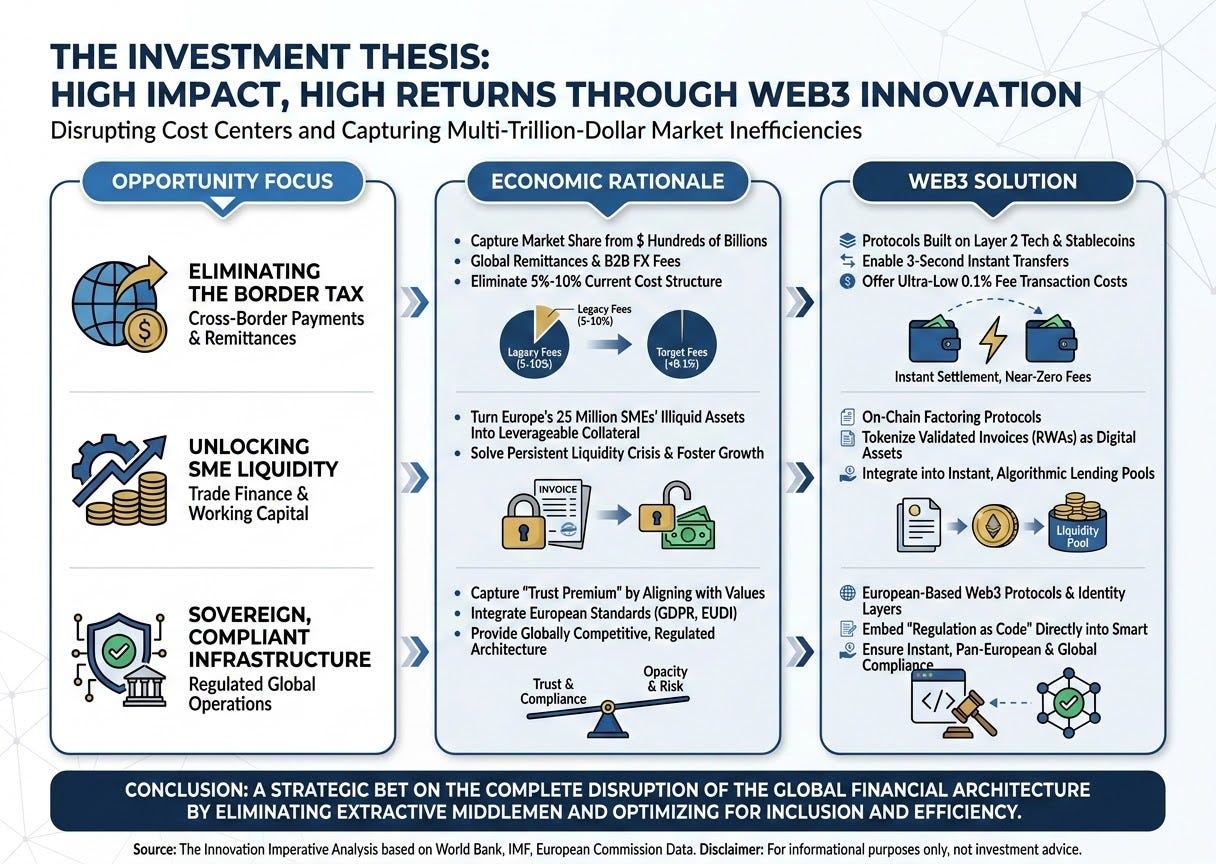

Despite the establishment of the Single Euro Payments Area (SEPA), high fees persist for cross-border transactions, especially for B2B payments and critical remittances sent outside the Eurozone. Migrant workers, who are essential to the economies of major EU states like Germany, France, and Italy, rely on these funds to support families abroad. Yet, they routinely lose a significant portion—typically between 5% to 10%—of their principal to fees, currency markups, and hidden costs levied by traditional intermediaries. This is a continuous, invisible wealth drain on the continent’s most financially fragile populations, directly contradicting the EU’s stated goals of social cohesion and global development leadership.

The SME Liquidity Crisis:

Europe’s backbone economy, consisting of roughly 25 million SMEs—which represent 99% of all businesses—is currently choked by slow, expensive access to working capital and trade factoring. Traditional financing processes are notoriously cumbersome, paperwork-heavy, and subject to national legal and regulatory fragmentation, which severely stunts the continent’s most vital growth engine. Crucially, the illiquid assets held by these SMEs (e.g., future invoices, inventory, specialized machinery) remain trapped, unable to be efficiently collateralized for rapid, affordable working capital, leading to predictable liquidity crises and suppressed growth.

The Web3 Solution for Europe is an architecture designed for seamless, sovereign integration. The convergence of the proposed Digital Euro (CBDC) with Web3 innovation creates an unprecedented opportunity to rapidly create a unified, ultra-low-cost financial infrastructure. Efficient Layer 2 solutions and the wholesale tokenization of Real-World Assets (RWAs) can immediately slash remittance and cross-border B2B fees to mere pennies and seconds. This immediate, frictionless movement of value would route billions of euros back to households and businesses. Furthermore, Decentralized Finance (DeFi) protocols can be utilized to tokenize assets like validated invoices, turning them into instant, borderless collateral for low-interest loans via permissioned DeFi pools, bypassing the cumbersome legacy banking system and finally achieving the promise of a truly efficient and financially inclusive Single Market. This immediate transformation represents the core of the $1 trillion economic opportunity.

III. The Developed Market Imperative: A Global Responsibility and Economic Necessity

Developed markets—the U.S. and the EU—must assume leadership in the innovation of financial inclusion. This is fundamentally not just a matter of correcting domestic issues; it is a profound global responsibility and a strategic economic necessity. The future of global finance, and thus global power, will be defined by the successful inclusion and empowerment of every participant, not just the privileged few.

The case for this leadership role is threefold and inextricably linked, demonstrating a virtuous cycle of domestic and global benefit:

Service the Domestic Underbanked to Foster Economic Resilience:

By aggressively adopting core Web3 architectural principles like Decentralized Identity and zero-cost payment rails, developed nations can finally provide truly equitable access to credit and services for their own marginalized populations, directly tackling the entrenched legacy of systemic discrimination head-on. A financially resilient domestic population—one not subject to the poverty tax of AFS—is an essential prerequisite for a stable, high-growth national economy. Moreover, the fundamental innovation required to solve inclusion for a community like South Central Los Angeles or the outer banlieues of Paris is precisely the same architectural innovation that unlocks scalable, equitable growth in Nairobi or Manila.

Uphold Worker Dignity and Security by Eliminating the Remittance Tax:

The vast, essential network of migrant and immigrant workers within developed markets relies heavily on cross-border remittances to support their families abroad. The crippling fees currently paid to intermediaries are essentially an invisible tax on labor and global family solidarity. Eliminating the 5-10% “Border Tax” on these transfers is an act of economic dignity and serves as one of the most powerful and stabilizing foreign policy tools available. When these workers are serviced with low-cost, high-speed, and securely verifiable transfer methods, the wealth they earn stays where it belongs—with their families—providing a crucial opportunity to build wealth and financial prosperity in emerging markets, which in turn has a direct, positive stabilizing effect on the global system.

Establish a Sovereign, Compliant Architecture for Global Export:

By leading with Web3 innovation, developed markets can create a next-generation financial operating system that embeds their values—such as robust data privacy (like GDPR in Europe) and strong consumer protection—directly into the underlying code layer, often called “Regulation as Code”. This results in a globally competitive, sovereign, and fully regulated architecture that can be exported worldwide. This process establishes a foundation for true, equitable global finance and captures the multi-trillion-dollar market currently lost to systemic inefficiency. Critically, if the West fails to lead in this architectural innovation, the space will inevitably be filled by alternative, less transparent, and potentially less accountable financial architectures, risking a loss of influence and competitive advantage.

IV. The Web3 Imperative: An Architecture for Equity and the Future of Finance

The reason the Web3 paradigm is the definitive, non-incremental answer to the financial inclusion challenge lies in its core architectural principles: decentralization, borderlessness, and transparency. These principles directly counteract the core failures of the traditional system—centralization, fragmentation, and opacity—enabling the creation of the financial infrastructure of the future. The ultimate goal is to eliminate the costly, extractive middleman entirely and create a system optimized solely for inclusion and efficiency. This is achieved through three architectural pillars:

Decentralized Identity (DID): The Passport to Global Finance

The ability to prove who you are and that you are financially reliable is the singular, most powerful gatekeeper in the legacy system. Traditional systems rely on centralized, revocable authorities: governments, banks, and opaque credit bureaus.

A Web3 DID system fundamentally shifts this power dynamic by allowing users to own their credentials (e.g., tax status, consistent rent payments, utility history) and selectively share them in a cryptographically verifiable way. This innovation removes the absolute reliance on national documentation, immediately solving the identification hurdles faced by immigrants and mobile citizens, aligning perfectly with initiatives like the European Digital Identity (EUDI). More importantly, it democratizes credit by tokenizing reliable, routine payments into verifiable credentials on a blockchain, giving the ‘credit invisible’ their first pathway to affordable capital and financial self-sovereignty.

Regulation as Code: Instant, Borderless Compliance

One of the most persistent and expensive barriers to financial innovation and scaling is the fragmented patchwork of national and regional regulations. A financial startup must spend millions on legal fees and dedicated compliance teams simply to scale its operations across multiple jurisdictions.

Smart Contracts revolutionize this constraint. By embedding essential compliance rules (such as Europe’s MiCA standards, or global AML/KYC guidelines) directly into the immutable, transparent code of the financial protocol, compliance is achieved by design. This paradigm shift creates instant, borderless compliance, dramatically reducing the cost and time required for scaling. It actively incentivizes pan-European and global growth while providing a highly auditable, technically enforced, and superior standard of consumer protection compared to opaque legacy systems.

Zero-Cost Rails: From Extraction to Value Creation

The fundamental philosophical and operational difference between Web3 and the legacy system is the cost model. Traditional finance is architected to extract maximum value through fees at every touchpoint—overdraft fees, cross-border transfer fees, maintenance fees, and FX markups. Web3, through technological advancements like efficient Layer 2 scaling solutions, minimizes the marginal cost of every transaction toward zero.

This means the cost of sending money across the globe becomes negligible, facilitating near-instantaneous transfers for mere fractions of a penny. This technological shift transforms what was a massive profit center for legacy intermediaries (high fees) into a universal, nearly-free utility for the user. The result is the direct routing of billions of dollars back into the hands of citizens, small businesses, and migrant families globally, boosting their financial power and dignity.

V. The Investment Thesis: High Impact, High Returns

For venture capitalists, corporate strategists, and governments, the Web3 Imperative is not a philanthropic endeavor; it is a high-impact, high-return investment thesis centered on capturing the multi-trillion-dollar market currently held hostage by systemic inefficiency. The thesis centers on three strategic vectors, all focused on disrupting existing cost centers:

This is not a bet on incremental growth in an already-saturated financial market, nor is it a marginal social issue. This is a bet on the complete disruption and replacement of the global financial architecture by eliminating the extractive middleman and creating a system optimized for inclusion and efficiency.

VI. Conclusion: Building the Financial Infrastructure of the Future

We have completed the circle: from identifying the inherent bias of the Walled Garden of global finance, to detailing the specific systemic failures in the U.S. and the $1 Trillion Crisis in Europe, the necessary path forward is singular and clear.

Financial Inclusion is the defining mission of our era precisely because it forces us to confront the core injustices and inefficiencies of the legacy system. It represents a dual, non-negotiable imperative: a moral necessity to lift the 1.4 billion unbanked and the millions of underbanked into full economic participation, and a monumental economic opportunity to unlock a colossal pool of potential wealth and GDP growth.

The Web3 Imperative provides the only architectural solution capable of meeting this challenge. By pioneering Decentralized Identity, building near-zero-cost payment rails, and democratizing access to capital through instant liquidity via tokenized assets, we are not simply building a slightly improved version of the old system; we are constructing a new, human-centric financial operating system for the entire world.

Entrepreneurs and investors must urgently shift their focus from the margins of fintech to the foundation of global finance. By committing to a decentralized, borderless, and trustless infrastructure, we can permanently eliminate the border tax, solve the SME liquidity crisis, and finally usher in an era of true, equitable financial inclusion—making finance sovereign, decentralized, and truly human-centric.

Sources & References

The World Bank, Global Findex Database: Source for the claim that “Roughly 1.4 billion adults worldwide remain completely unbanked, representing about one-third of the global adult population” and the overall 69% account ownership statistic.

Global Findex DatabaseInternational Monetary Fund (IMF): Source for the claim that “Boosting financial inclusion is positively associated with GDP growth, by up to 14% in developing economies.”

IMF Staff Discussion Notes on Financial InclusionConsumer Financial Protection Bureau (CFPB): Source for the claim regarding the high cost of Alternative Financial Services (AFS) in the U.S., specifically that a typical two-week payday loan can carry an equivalent Annual Percentage Rate (APR) of “300% to 400%.”

CFPB: Research and ReportsFederal Deposit Insurance Corporation (FDIC) & Consumer Financial Protection Bureau (CFPB): Joint sources for the discussion on U.S. “banking deserts,” algorithmic discrimination, and the legacy of redlining impacting access to fair credit for minority and LMI households.

FDIC: Household Survey on Banking and Financial Services | CFPB: Policy and ComplianceThe World Bank (Remittance Price Data) & Pew Research Center: Sources for the claim about identification barriers and the “remittance tax,” stating that migrant workers often lose “5% to 10% of their principal to fees and markups” on international money transfers.

World Bank: Remittance Prices Worldwide | Pew Research Center: U.S. Immigration and BankingThe Brookings Institution: Source for the discussion on the “Poverty Tax” and how Low-to-Moderate Income (LMI) households are forced out of the traditional banking system due to minimum balance requirements and overdraft fees.

Brookings Institution: Economic Policy ResearchEuropean Commission: Source for the statistic regarding the number of Small and Medium-sized Enterprises (SMEs) in Europe, stating Europe has “25 million SMEs—the economic backbone,” which are constrained by slow, expensive access to capital.

European Commission: SME Definition and Policy