The Digital Euro Dilemma: Why Web3 is Essential to Avert a $1 Trillion Financial Meltdown in the EU

The Looming Crisis of a Fragmented Financial Future

The conversation about financial exclusion has been dominated by the challenges in the developing world or the nuances of the US “underbanked” problem. But the European Union, a beacon of modern economic and social policy, harbors a massive, silent divide that represents both a profound moral failure and an untapped economic opportunity easily exceeding $1 trillion in potential wealth generation.

This article, following my previous explorations into the “Walled Garden” of finance and the “Web3 Imperative” in the US, pivots the focus to the heart of the single market. The failure of the legacy system in the EU is not the same as in America, yet its impact is just as corrosive: it is a fragmentation of financial services across borders, a deep reliance on expensive, non-European payment rails, and a systemic lack of access to affordable, next-generation financial tools for millions of citizens and businesses, particularly Small and Medium-sized Enterprises (SMEs).

We are not going to solve this by building another incremental fintech app or by tweaking the existing SEPA framework. The scale of the challenge—and the size of the opportunity for forward-thinking investors and entrepreneurs—demands a decentralized, borderless, and low-cost financial infrastructure. The solution is the Web3 Imperative for Europe, a movement that aligns perfectly with the strategic goals of the proposed Digital Euro, turning it from a mere public-sector alternative into the foundational layer for a fully inclusive, competitive, and unified European digital economy.

Quantifying the Divide: Europe’s Hidden Financial Exclusion

The narrative of universal financial access in the EU is largely a myth. While most citizens have a bank account, access to equitable, borderless, and affordable financial services is far from guaranteed. This is a multi-layered problem of affordability, technological fragmentation, and market access that is crushing economic potential across the bloc.

The State of Exclusion: Fragmented Access and the Cost of Cross-Border Payments

The challenge in the EU often masks itself not as a lack of account ownership, but as a severe inefficiency in fundamental transactional services.

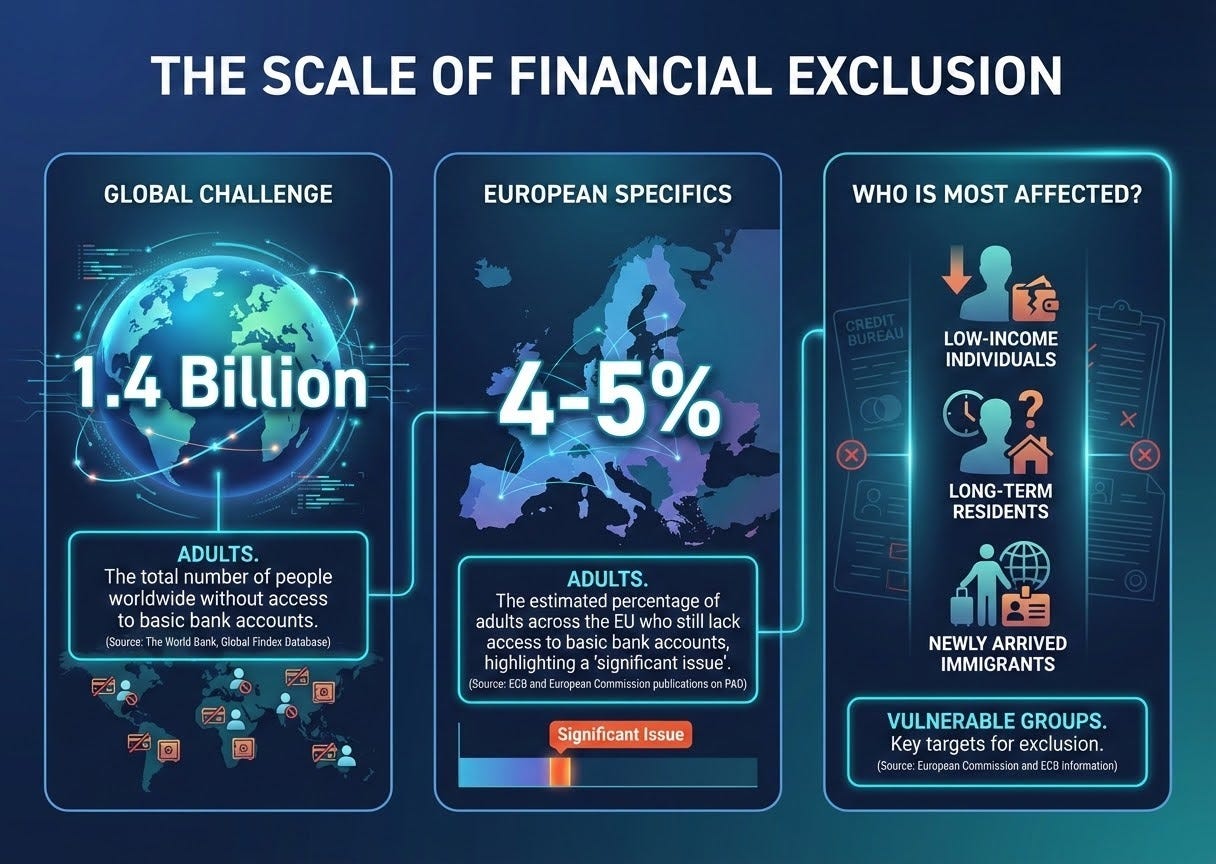

A. The Basic Payment Account Problem

Despite the EU’s Payment Accounts Directive (PAD) ensuring all residents have a right to a basic payment account, millions of people still struggle. According to the European Commission, a lack of access to formal banking services remains a significant issue in many Member States. While official “unbanked” rates may appear low compared to global averages, the sheer scale of the population is significant:

Source: The World Bank, European Commission publications.

B. The Border Tax: A Drain on the Single Market

The Single Euro Payments Area (SEPA) aimed to unify payments, but it has not eliminated the high cost of cross-border transactions, especially for remittances and business-to-business (B2B) payments that exit the SEPA zone or rely on inefficient correspondent banking.

When migrant workers send money to non-EU nations, the “remittance tax” is a massive wealth drain. Fees and exchange rate markups can consume 5% to 10% of the principal amount. The global market for these transfers is measured in the hundreds of billions, and the portion flowing out of the EU is a significant, continuous drag on citizens’ income. Web3, through stablecoins and efficient Layer 2 solutions, can reduce these costs to mere pennies, directly routing billions of euros back to households.

C. The SME Liquidity Crisis

The financial fragility of Europe’s 25 million SMEs—which are the backbone of the European economy, employing two-thirds of the private sector workforce—is another massive pain point. SMEs consistently cite access to finance and cross-border payment efficiency as major obstacles.

Factoring and Invoice Financing: SMEs often face high costs and slow settlement times for invoice factoring, a crucial tool for managing cash flow. Traditional processes are cumbersome and subject to national legal fragmentation.

Lack of Collateralized Digital Assets: Unlike large corporations, many SMEs lack the accessible digital assets to collateralize loans quickly and affordably.

Web3 and Decentralized Finance (DeFi) offer solutions here by tokenizing real-world assets (RWAs)—such as future invoices or inventory—to create instant, borderless liquidity solutions that bypass the slow, expensive legacy banking system.

The Web3 Imperative for European Competitiveness

The $1 trillion economic opportunity lies in eliminating the cumulative cost of these inefficiencies and barriers: the cross-border transaction tax, the cost of delayed liquidity for SMEs, and the fees extracted from financially fragile populations. This requires an infrastructure designed for inclusion and borderlessness—the core value proposition of Web3.

A. Decentralized Identity (DID): The Passport to Financial Access

For millions of mobile Europeans, cross-border financial life is a bureaucratic nightmare. Opening a bank account in a new Member State, accessing consumer credit, or establishing a business requires redundant Know Your Customer (KYC) checks and often favors local residents.

The EU’s own push for a European Digital Identity (EUDI) is a perfect alignment with the Web3 concept of Decentralized Identity (DID). A self-sovereign, digital identity, secured by a blockchain, would allow a user to prove their identity and verifiable credentials (like tax status, educational background, or consistent rent payments) without relying on a centralized national database or a traditional bank.

This paradigm shift would:

Simplify Cross-Border Onboarding: Allow a citizen to instantly and compliantly access a loan, insurance, or payment account anywhere in the EU.

Unlock Credit for “Thin File” Citizens: Tokenize reliable, routine payments (rent, utility bills) into verifiable, permissioned credentials, bypassing traditional credit bureaus and democratizing credit scoring for millions of “credit invisible” individuals.

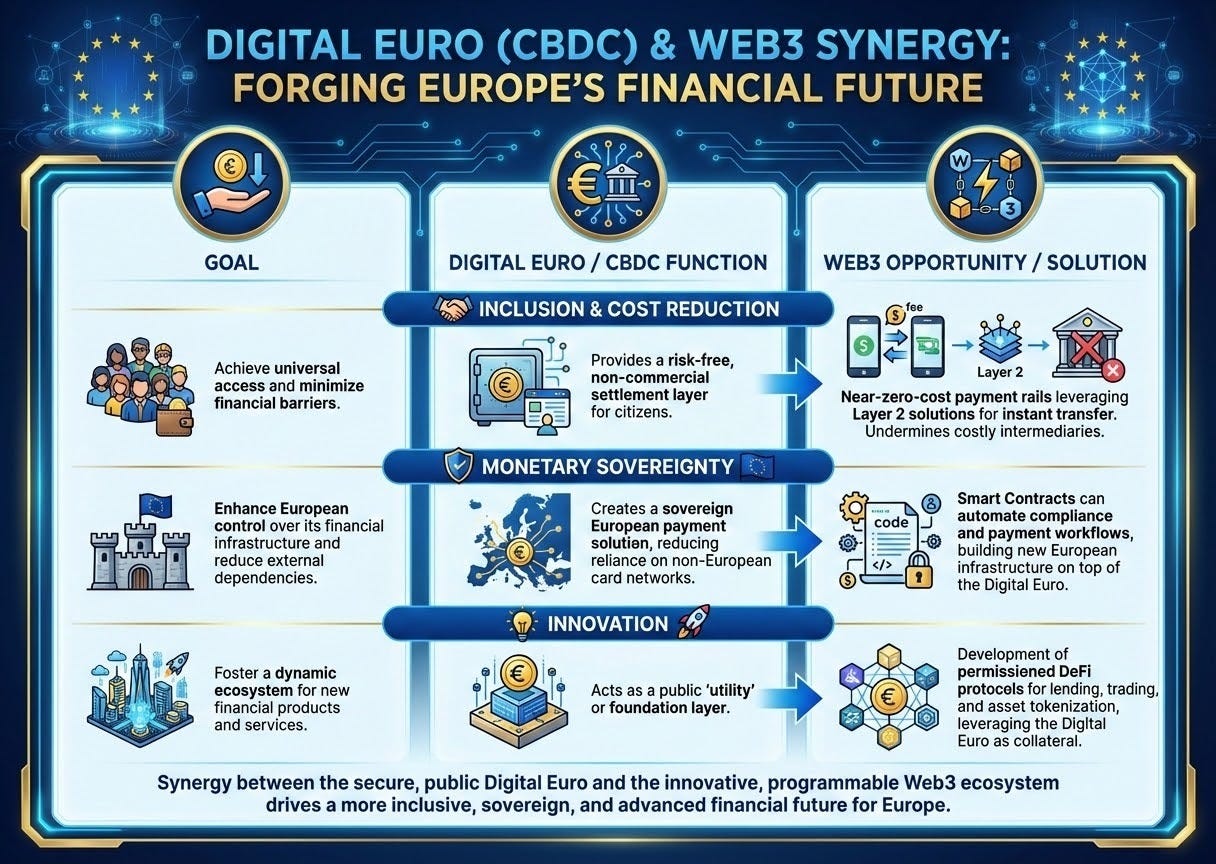

B. The Digital Euro and the DeFi Nexus

The European Central Bank (ECB)’s proposal for a Digital Euro, a Central Bank Digital Currency (CBDC), is the single most important policy development for European financial inclusion. The ECB explicitly aims for the Digital Euro to be a public-sector alternative to private-sector digital payment systems, with the goal of providing a free and privacy-protected payment option to foster inclusion.

This public-sector initiative creates a massive infrastructure opportunity for Web3 innovators.

The opportunity for founders: Build the next generation of financial services—from micro-lending to tokenized invoice financing—directly on top of the Digital Euro infrastructure. This allows for innovation that is both compliant by design and inherently low-cost.

C. Disrupting the Regulatory Fragmentation

The current financial landscape is a patchwork of national regulations that hinder cross-border scaling for startups. A company building a lending product in Germany faces an expensive and time-consuming adaptation process to launch in Italy.

Smart contracts, as the ultimate embodiment of “regulation as code,” can revolutionize compliance. By embedding EU-wide rules (like MiCA, AML/KYC) directly into the protocol’s code, Web3 solutions can achieve instant, borderless compliance. This reduces the cost of scaling for startups, incentivizing pan-European growth and directly boosting innovation and competition. The transparency and immutability of the blockchain become the ultimate tool for consumer protection, offering a higher standard of trust than opaque legacy systems.

Investment Thesis: High Impact, High Returns

For venture capitalists and corporate executives, the investment thesis in European financial inclusion is a multi-layered one, yielding both significant profit potential and strategic regional impact.

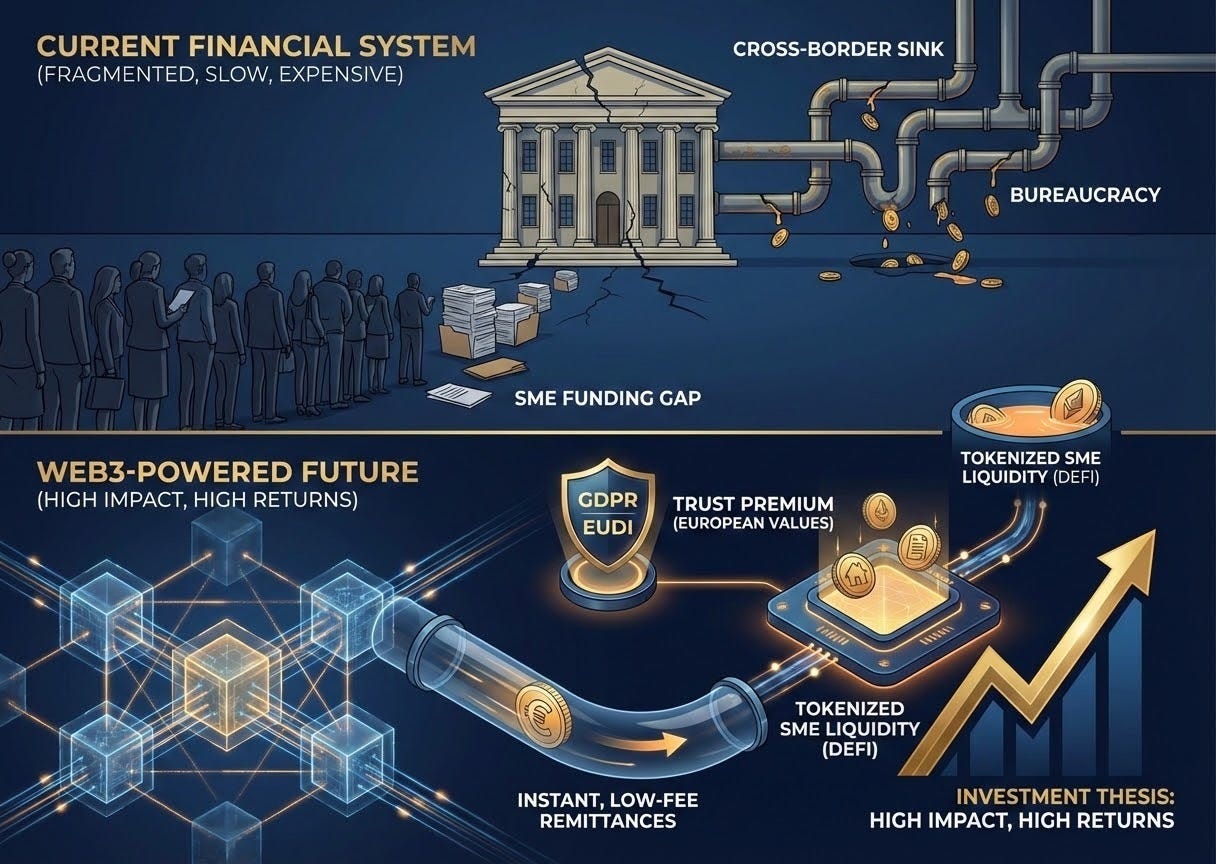

1. Capturing the Cross-Border Payment Sink

The market for international remittances and SME cross-border B2B payments is fragmented and lucrative for current intermediaries. A Web3 platform that can leverage stablecoins or a future Digital Euro to offer 3-second, 0.1% fee transfers between European citizens and non-EU countries will capture massive market share. This is not an incremental improvement; it is a complete disruption of the current business model.

Opportunity Focus: Remittance platforms, B2B cross-border payment protocols, and FX providers built on Layer 2 tech.

2. Unlocking SME Liquidity

Europe’s millions of SMEs represent an immense, under-leveraged collateral base. The company that successfully builds a protocol to securely tokenize SME assets (e.g., future earnings, validated invoices, real estate) and uses them as collateral for low-interest, instant loans via permissioned DeFi pools will fundamentally transform European business financing. The current lending model is slow, expensive, and risk-averse. The Web3 model is instantaneous, algorithmic, and transparent.

Opportunity Focus: Tokenized asset platforms, on-chain factoring, and automated treasury management tools for SMEs.

3. The Trust Premium

Europe places a high premium on data privacy and sovereignty, making the current reliance on non-EU tech giants and payment networks a long-term strategic risk. Investments in European-based Web3 infrastructure—protocols, identity layers, and core blockchain technology—that adhere to GDPR and align with the EUDI framework will capture a “trust premium” from both consumers and regulatory bodies. The future of European finance must be built on European values.

Conclusion: The Defining Mission for a Digital Europe

Europe’s financial system is at a critical juncture. The promise of the Single Market remains unfulfilled for millions of citizens who face fragmented access, and for millions of SMEs suffocated by slow, expensive payments and a lack of liquidity. This is an economic failure with a price tag far exceeding $1 trillion in lost GDP and potential wealth.

The path forward is clear: it is the Web3 Imperative coupled with the strategic vision of the Digital Euro. Entrepreneurs and investors must shift their focus from building marginal improvements to building the foundational financial infrastructure for the next generation. By leveraging Decentralized Identity, smart contracts, and efficient, near-zero-cost payment rails, we can bypass the legacy system’s walled gardens, eliminate the border tax, and usher in an era of true, equitable financial inclusion—making Europe the global leader in sovereign, decentralized, and human-centric finance.

Data and Statistics Sources

Global Unbanked Figures: For global context on financial exclusion, highlighting the scale of the issue worldwide. Source: The World Bank, Global Findex Database.

EU Underbanked Data: The World Savings and Retail Banking Institute

Basic Payment Account Access in the EU: Reference to the EU’s recognition of persistent access issues. Source: European Central Bank (ECB) and European Commission publications related to the Payment Accounts Directive (PAD).

Remittance Costs: Data on the high cost of cross-border money transfers. Source: Various reports from the World Bank and the Consumer Financial Protection Bureau (CFPB) on remittance taxes and fees.

SME Economic Role: Statistics on the size and contribution of Small and Medium-sized Enterprises in the European economy. Source: European Commission official documentation and SME Fact Sheets.

Digital Euro Initiative: Reference to the public-sector goals of the proposed Digital Euro, specifically regarding inclusion. Source: European Central Bank (ECB) publications and proposals (e.g., [https://www.ecb.europa.eu/paym/digital_euro/html/index.en.html](https://www.ecb.europa.eu/paym/digital_euro/html/index.en.html)).

EUDI (European Digital Identity): Reference to the EU’s push for a common digital identity framework. Source: European Commission information on the European Digital Identity Wallet.

GDP Growth and Financial Inclusion: The positive correlation between boosting financial inclusion and GDP growth. Source: IMF (International Monetary Fund) articles and reports on financial development (e.g., https://www.imf.org/en/Publications/fandd/issues/2016/june/caruana).